So, the wizards at the Federal Reserve finally waved their little wands and graced us with a rate cut. The headlines are practically screaming it. Mortgage Rates Drop Again, At Lowest Level In A Year. Pop the champagne, I guess? The average rate for a 30-year fixed loan is now a breezy 6.156%. That’s a whole… checks notes… one basis point lower than a week ago.

Give me a break.

This is the financial equivalent of a doctor telling a guy with a sucking chest wound to take an aspirin. We’ve been suffocating under rates hovering near 7% for what feels like an eternity. For anyone under 40 who didn't luck into a house during the pandemic-fueled fever dream of 2.65% rates, the American Dream has felt more like a hostage situation. And now we’re supposed to celebrate this microscopic dip?

I can just picture it: a young couple hunched over their laptop at the kitchen table, the glow of a `mortgage calculator` illuminating their exhausted faces. They plug in the numbers for a starter home that costs more than their parents' last three houses combined, see the new, "lower" monthly payment, and realize it's still a thousand dollars more than they can afford. This ain't a rescue mission; it's just rearranging the deck chairs on the Titanic.

The Experts Are Peddling Nostalgia, Not Solutions

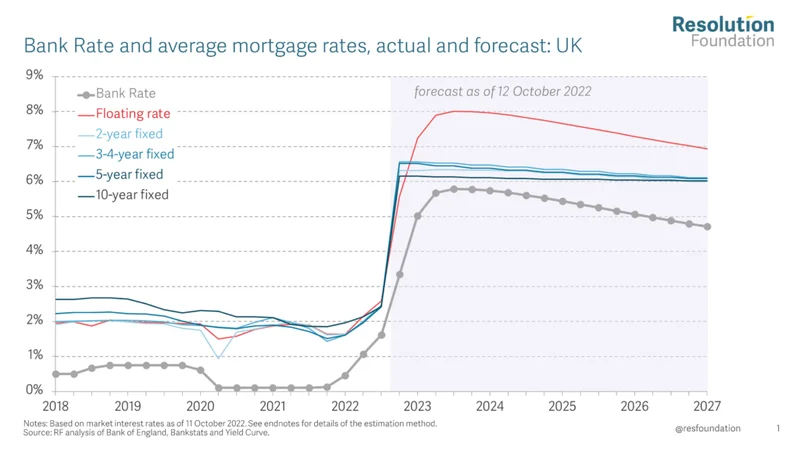

Every time `current mortgage rates` get painful, the financial media trots out the same tired line. They pull up some dusty chart from the St. Louis Fed and point to 1981, when rates were over 18%. "See?" they say, with the smug satisfaction of a high school history teacher. "It's not that bad! Historically, this is normal!"

This argument is just lazy. No, 'lazy' doesn't cover it—it's a deliberate, insulting misdirection. Comparing the `interest rates today` to the rates of 1981 without mentioning that the median home price back then was about $68,000 is completely disingenuous. You could buy a house with a good salary and a firm handshake. Today, the median price is astronomically higher, and wages have stagnated into a puddle of despair.

Are we seriously supposed to find comfort in the fact that our parents had it worse for a brief, weird period forty years ago? How does that help a millennial with $80,000 in student debt trying to compete with all-cash offers from private equity firms buying up entire neighborhoods? It doesn't. It's a narrative designed to make you feel ungrateful for being crushed by a system that's fundamentally broken.

And the advice they give is always the same. "Get your credit score up to 740!" "Lower your debt-to-income ratio!" Thanks, Captain Obvious. That's like telling someone stranded in the desert to "just find an oasis." It completely ignores the systemic rot and places all the blame squarely on the individual for not being perfect enough to participate in a rigged game. Everyone is hoping for better `refinance rates`, but offcourse they are, the current situation is untenable for most people.

Don't Bet on a Soft Landing

So what happens now? The Fed made a cut. There are a couple more meetings on the calendar this year. The market seems to think this is the beginning of a beautiful new chapter of relief. I’m not buying it.

This whole economic machine feels like a Jenga tower where we've been pulling out the wrong blocks for a decade. The Fed’s rate cut is less a strategic move and more a desperate prayer. They're trying to thread a needle in a hurricane. On one side, you have persistent inflation, a massive national debt, and the political wildcard of a Trump administration that could throw gasoline on the fire with tariffs and trade wars. On the other, you have mounting layoffs and the very real threat of a recession they've been trying to wish away.

The real monster under the bed isn't even the federal funds rate everyone obsesses over. It's the Fed's balance sheet. For years, they were buying up mortgage-backed securities like a drunken sailor on shore leave, artificially keeping rates low. Now they’re letting those assets shrink, which puts upward pressure on `home mortgage rates`. So while they cut with one hand, they’re still tightening with the other.

What does that mean for you? It means uncertainty. It means this little dip might be all we get for a while. It could even be a head-fake before things get worse. Then again, what do I know? Maybe I'm just a cynic. Maybe this really is the turning point and we'll all be looking at amazing `refinance mortgage rates` in a year. But I sure as hell wouldn't bet my financial future on it.

This Is Just Lipstick on a Pig

Let's be brutally honest. This quarter-point cut doesn't fix a thing. It’s a PR move. It’s a sedative for the markets. It is not a solution for the generation of Americans locked out of homeownership. The fundamental problem—wildly inflated home prices, stagnant wages, and a financial system that prioritizes corporate profits over human stability—remains completely untouched. Celebrating this tiny dip in `30 year mortgage rates` is like celebrating that your fever went from 104 to 103.8. You're still sick, and the underlying disease is only getting worse.